Heads up: Our 2026 State of Fintech report will be out next Tuesday. Sign up today for a deep dive with the F-Prime team on February 24th.

Welcome back to Fintech Prime Time, where we share data-driven insights from the F-Prime Fintech Index. This month, we’re focused on two things investors care about most right now: fintech’s strong finish for H2 2025, and the performance of newly listed companies. We will also analyze the data on fintech valuations and revenue multiples as the market normalizes.

Meet the Fintech Index’s Q4 Additions

By Abdul Abdirahman and Andrew Chen

Q4 marked one of the most active periods for index refreshes since the post-2021 reset. The F-Prime Fintech Index expanded from 47 to 54 companies, reflecting five new venture-backed exits and two re-listings, driven by a steady reopening of the IPO window and a backlog of scaled, venture-backed fintechs finally coming to market.

New Additions

Re-Listings

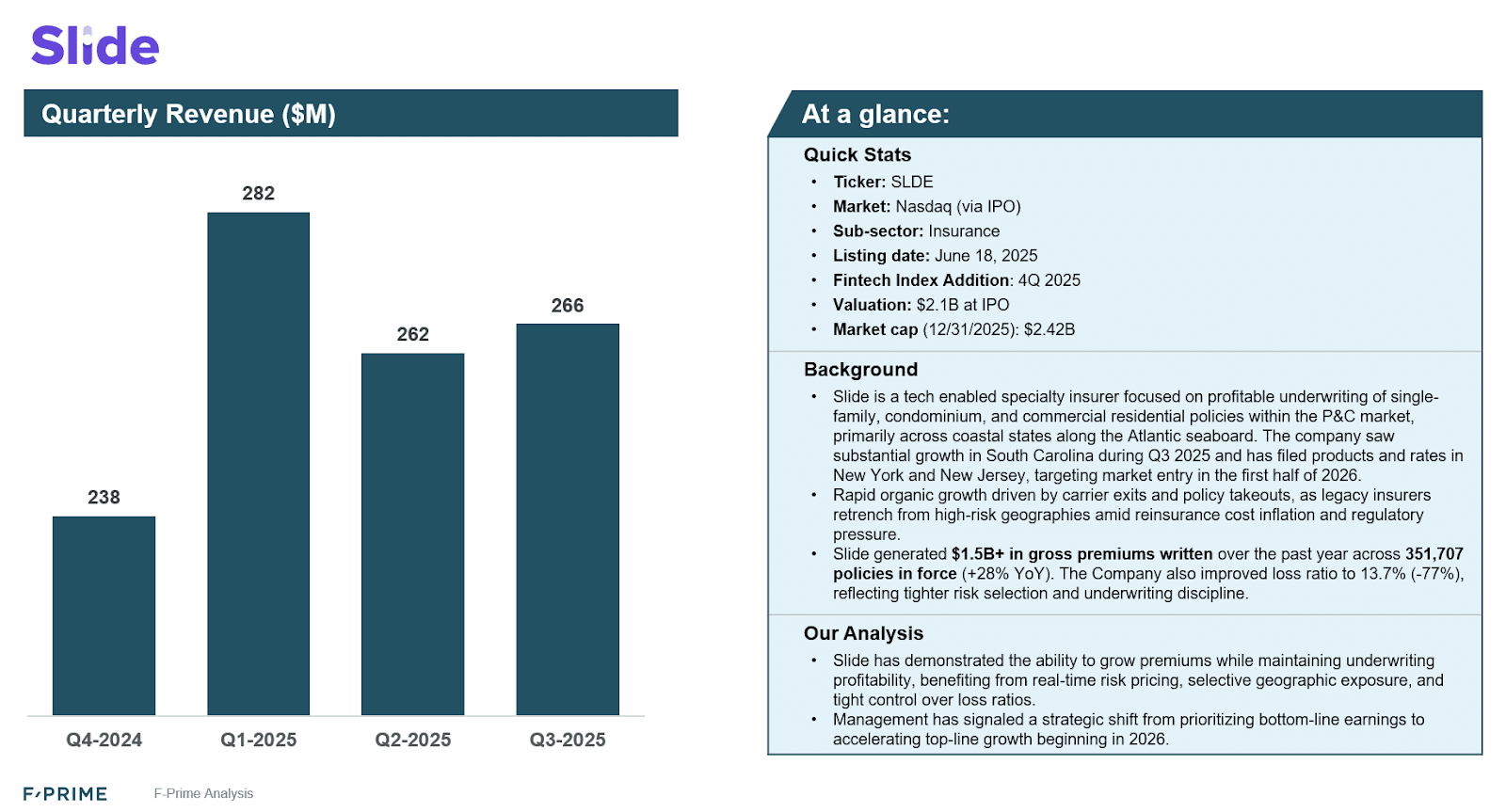

Dave (Banking)

Dave was first added to the Index when it went public via a SPAC merger in January 2022. Dave is a neo-bank and lending platform and went public at ~$3B marketcap. The company faced early market challenges with its market cap dropping to as low as $55M by mid-2023. Due to the company not meeting the criteria for inclusion in the Fintech Index, we removed it. In a little over a year, Dave’s market cap has rebounded from $500M in Nov. 2024 to ~$3B, where it closed 2025. This growth in share value is largely driven by Dave’s improving fundamentals in 2025. The Company saw strong quarterly revenue growth (+63% yoy to Q3 2025) and surging adjusted EBITDA, which more than tripled to $58.7M in Q3. These improvements are directly linked to the success of its proprietary CashAI underwriting model, which has helped expand profit margins and maintain low loan delinquency rates, proving that the company’s AI investments are paying off.

Root Inc. (Insurance)

Root was first added to the Index when it went public in October 2020 at ~$7B market cap on $200M revenue run-rate. While Root continued to grow revenue as a public company reaching nearly $500M by 2023, in 2024 revenue nearly tripled to $1.2B while also achieving profitability ($31M). Strategic reduction in reinsurance cessions played a big role. In 2024 Root dramatically lowered its cession rate from 37.1% to ~13.0% in 2024. In 2025 the company continued to show signs of improving fundamentals, with efforts focused on growing revenue and profitability within the competitive insurance market. Root currently has a market cap of $1.1B and has been added back to the Index.

On Deck

Two recently listed companies are now seasoning for potential inclusion in Q1. We will share more about them at the end of Q1.

Navan (NAVN) – Travel, payments, and expense management (eligible January 2026)

Wealthfront (WLTH) – Digital wealth management (eligible March 2026)

Q3 Index Performance: What the Data Actually Says

Despite lingering skepticism around fintech valuations, the F-Prime Fintech Index tells a more nuanced story.

Key Takeaways

-

On October 30th, the Index performance nearly matched its 2021 peak: +1,6537% vs. +1,702% during the prior cycle high.

-

Meaningful index breadth expansion: The addition of more Lending and Wealth/Asset Management companies to the index signals healthier public market participation and broader diversification.

-

Aggregated fintech revenue multiples averaged 5.6x, broadly flat year-over-year and down from 6.2x in Q3.

This is not a return to 2021 excess. Instead, it is a market repricing risk more rationally as companies continue to improve their underlying fundamentals. Over the past years many of the Fintech Index companies have marched towards or achieved profitability while maintaining 20%+ YoY revenue growth, sometimes at massive scale. We will explore this further in our upcoming State of Fintech report to be released next month.

Notable Multiple Movements

Banking – 5.6x (down from 8.1x)

The headline driver here is Circle, whose revenue multiple compressed sharply from 22x to ~7.3x after its public listing in June. This reset pulled down the broader banking cohort, even as underlying growth remained intact.

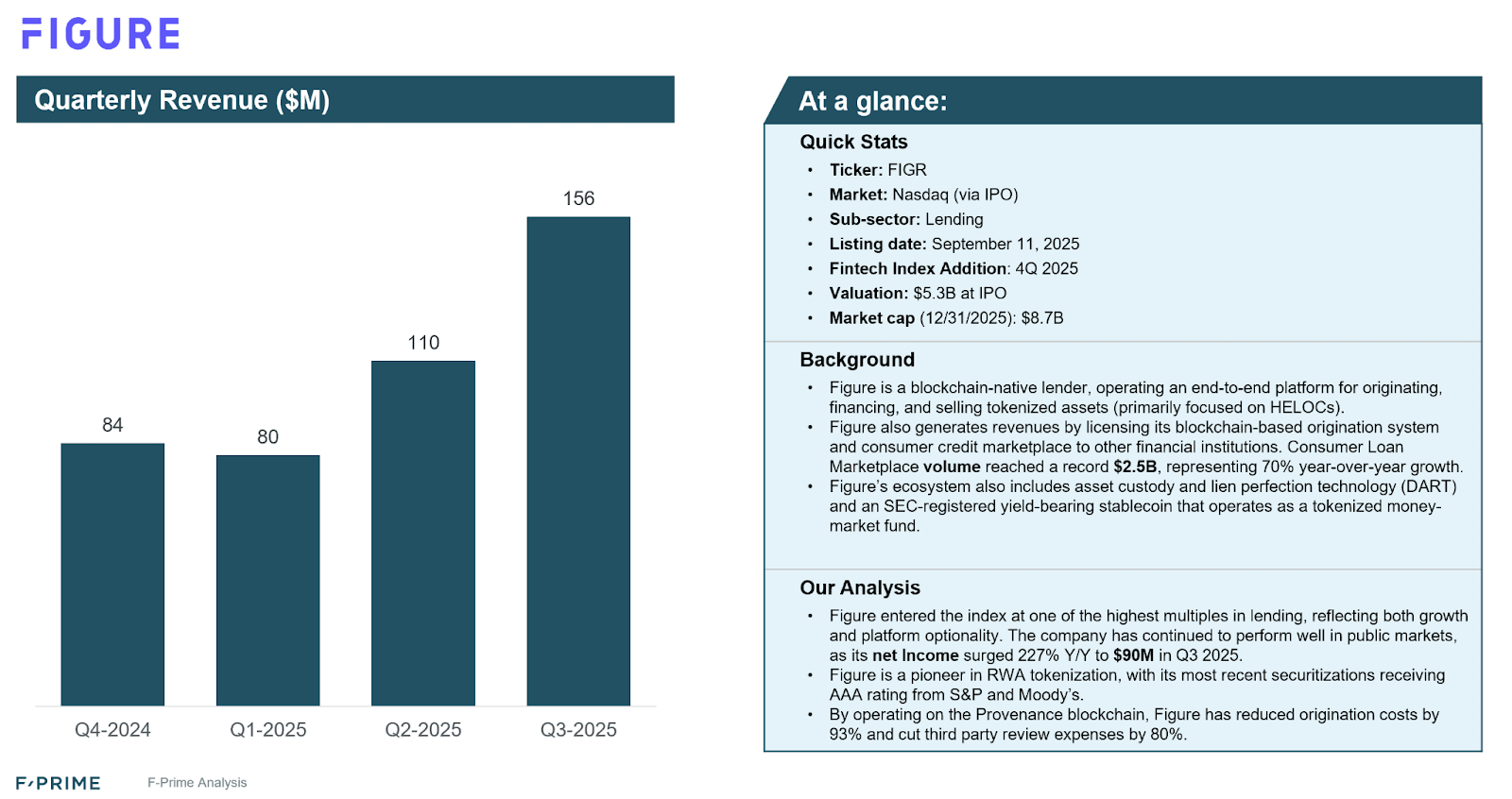

Lending – 7.2x (up from 5.9x)

Lending multiples expanded, largely due to new inclusions. Figure entered at ~21.5x revenue multiple, lifting the category average and reinforcing a broader trend: platform-driven lenders with differentiated infrastructure continue to command premiums.

The Bigger Picture on Valuations

High multiples at IPO are not new, especially for category leaders exiting private markets after prolonged growth phases. What is consistent is what follows: multiples tend to converge toward peer averages over time, with a modest premium reserved for companies that continue to outgrow the cohort.

That pattern is clearly re-emerging. The public market is once again rewarding durable growth, scale, and operating leverage — but without forgiving execution risk.