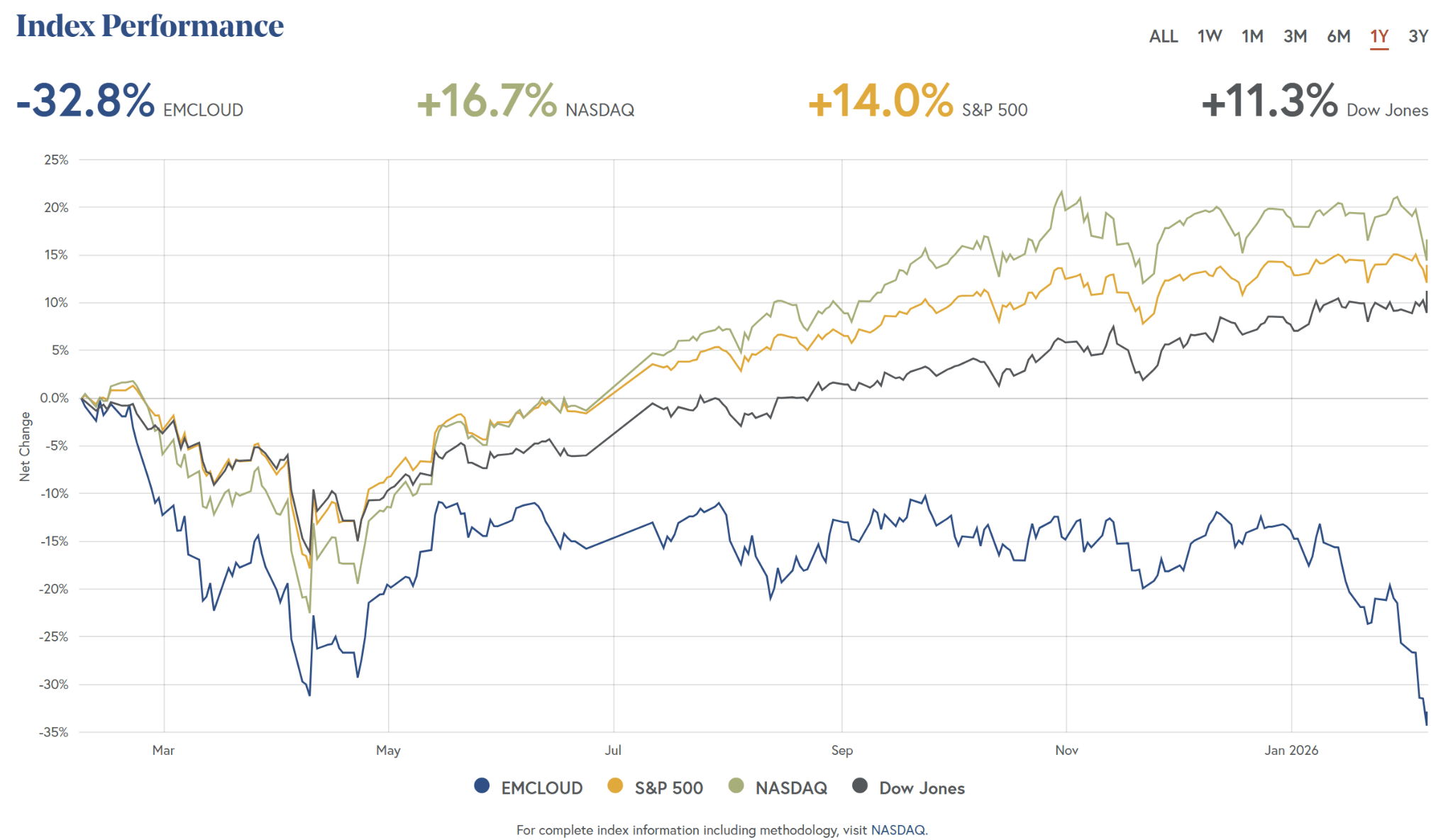

Four years ago, I wrote about the “SaaSacre of 2022” when SaaS companies were pummeled in the public markets, largely as a consequence of macro drivers such as rising interest rates. Fast forward to today, and we’re in the midst of another brutal SaaS sell-off (chart below). Tuesday of this week was particularly unforgiving as a single product announcement from Anthropic sent the public markets into a tailspin that wiped out hundreds of billions of market value from SaaS stocks.

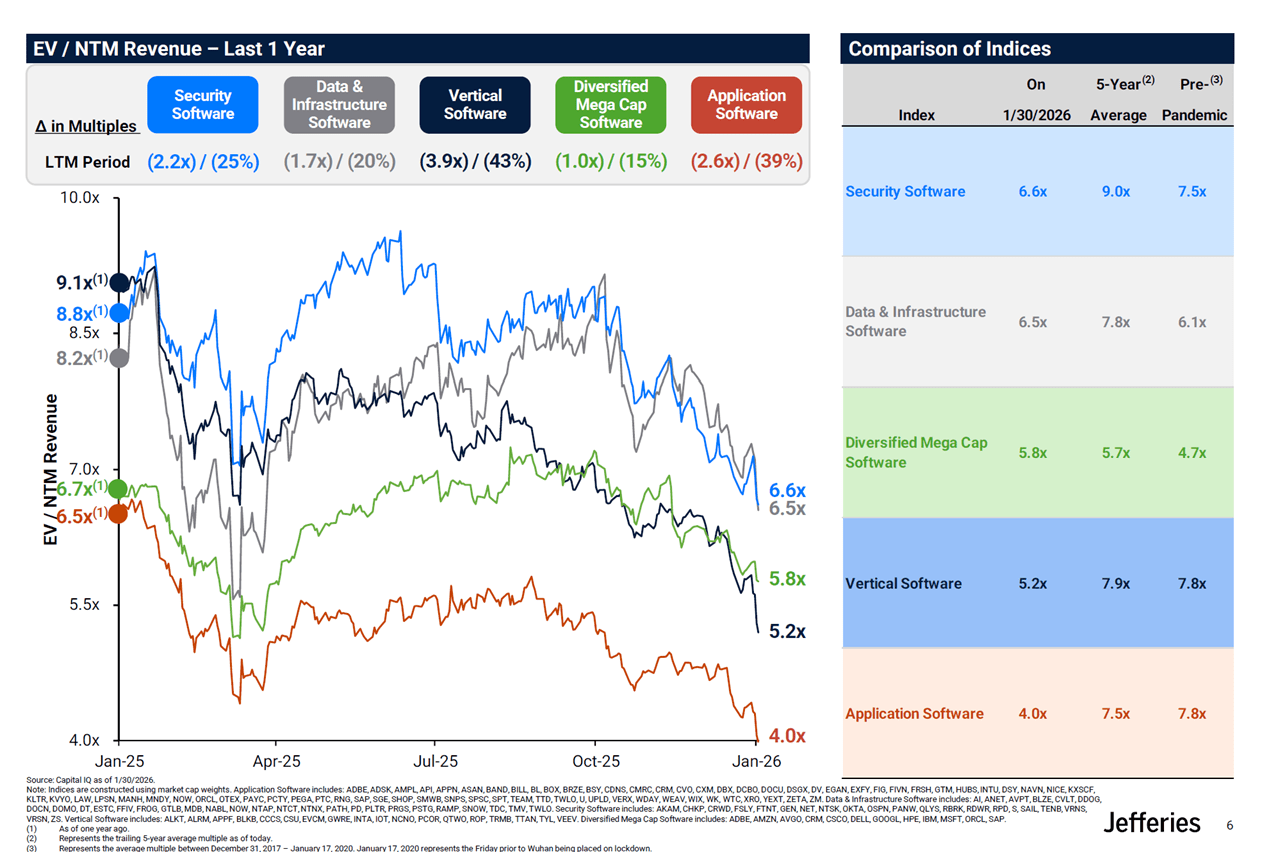

The current SaaSacre’s defining characteristics are strikingly different from 2022. For one, unlike in 2022 where unfavorable macro conditions had a negative blanket effect across all public market indices, we’re now seeing SaaS multiple compression to historical lows despite favorable macro indicators supporting exuberance in other market categories:

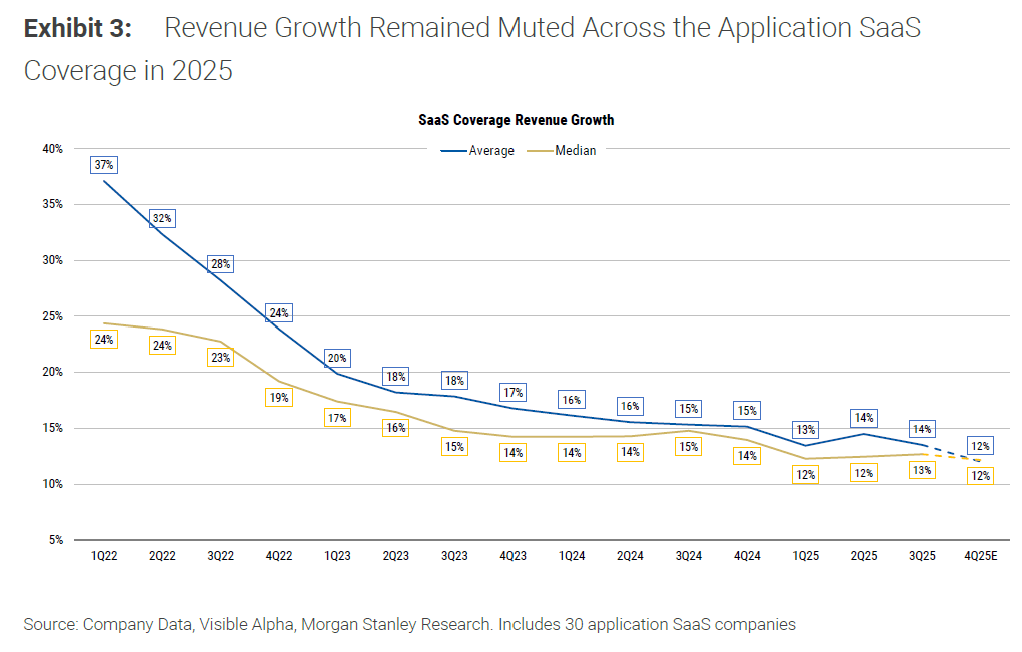

Additionally, fundamental metrics like growth rates and net dollar retention are muted across the SaaS cohort today, unlike in 2022 when underlying fundamentals remained largely intact:

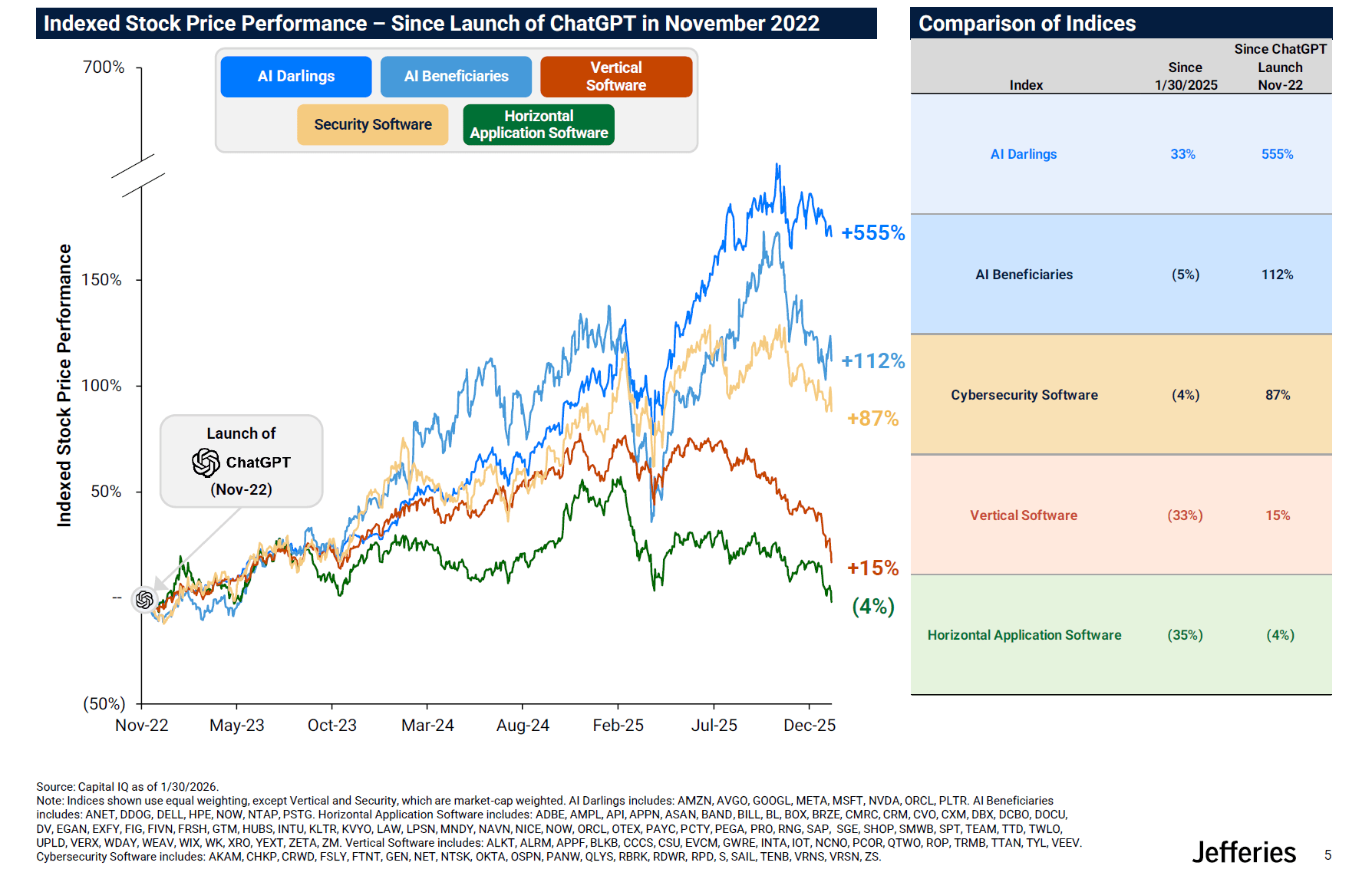

Lastly, different from the rapid market reactivity seen in 2022’s SaaSacre, the current pullback has been part of a slow-burning “Death of SaaS” sentiment shift (particularly against vertical and horizontal applications) that has taken hold in the software landscape since the launch of ChatGPT:

AI-related concerns at the center of 2026’s SaaSacre

2026’s SaaSacre has been a hot-button topic among VCs, and the discussion has been extremely multi-faceted. Simply proclaiming that “AI is killing SaaS” does not capture the full nuances of the debate. Here is my summary of the biggest AI-related fears driving the current SaaSacre:

Terminal value and growth impacts:

-

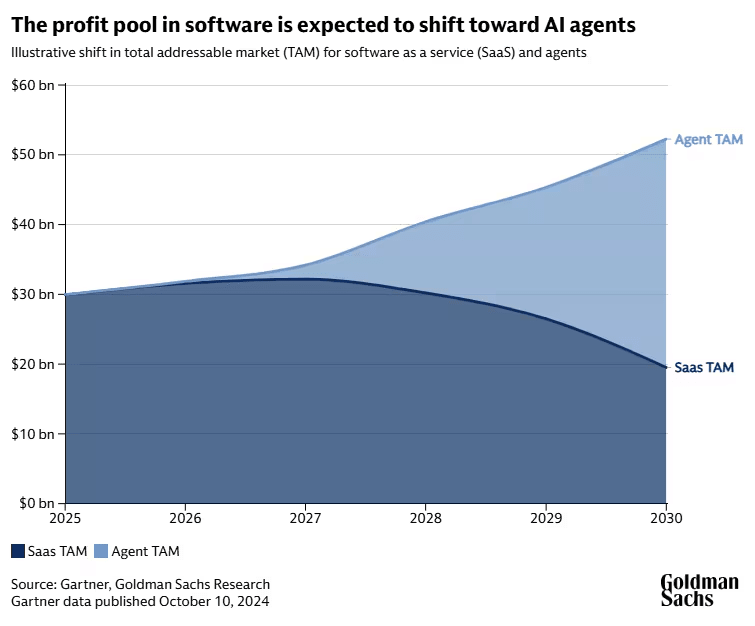

AI disruption could make SaaS obsolete and reduce terminal value: Next-gen AI and agentic players pose an existential threat to incumbent SaaS vendors (chart above), particularly in software categories such as customer support, go-to-market tooling, content creation, and coding, where AI is already causing rapid disruption of the stack.

-

AI collapses workflow complexity: AI agents are starting to consolidate workflows and click-paths, bypassing incumbent SaaS UIs and reducing user engagement with those surfaces. For instance, users can now query and execute actions across different software platforms through natural language prompts in a chat box. Computer use is another example. This factor is highly disruptive to UI-first (vs. API-first) incumbents.

-

Agentic layer could displace value from systems of record: Related to the point above, there is deeper debate going on around AI agents potentially “hollowing out” siloed systems of record. Microsoft’s CEO Satya Nadella first sparked this debate by characterizing apps as a business logic GUI on top of CRUD (Create, Read, Update, Delete) databases that could be collapsed as value begins accruing to an agentic layer that can be multi-repo CRUD. This factor has disproportionately impacted legacy systems in areas such as customer relationship management and enterprise resource planning.

-

Decreasing cost of software development could tip the scales toward “build” rather than “buy”: With vibe coding tools, it is now easier than ever to create software with AI. This may push companies to build more custom software in-house instead of buying from third-party vendors, especially for point solutions.

-

AI could structurally flatten out the SaaS growth curve: As highlighted earlier, growth of the incumbent SaaS cohort has already been muted. This is somewhat unsurprising since growth tends to slow as market adoption S-curves mature, compounded by factors like app fatigue. Now, AI adds a new layer of pressure on growth deceleration. Incremental IT budgets are overwhelmingly flowing to AI-native vendors. Even enterprises not fully invested in AI are waiting to see what next-generation players can deliver, which could slow down their software spend in other areas. Meanwhile, AI-native companies are showing unprecedented growth and product velocity at a level that existing players cannot match, leaving incumbents looking laggard and dated.

Profitability impacts:

-

Decreasing cost of software development could lead to cheaper competitors flooding the market: As the marginal cost to build software goes to zero with AI, this could lead to price pressures and lower ACVs for incumbents if AI enables more and/or cheaper alternatives to enter the market. Furthermore, if AI coding makes it easier for competitors to get to parity or makes it easier to migrate tools over to competitors, this could lead to higher churn and higher CAC.

-

AI drag on gross margins: Even if SaaS incumbents incorporate AI into their products, this could lead to lower gross margins than historical cloud benchmarks since AI revenue is structurally more expensive due to compute, model API costs, etc.

-

Talent wars: Competition for AI talent could exacerbate SBC expenses for incumbents. As SBC overhang worsens, long-term profitability could be impacted:

Business model impacts:

-

Seat-based pricing under pressure: SaaS pricing has historically relied on the number of users or licenses as a proxy for value delivered. Many SaaS incumbents thus leverage seat-based pricing. If AI agents end up doing a substantial amount of white collar work in the enterprise, this could reduce monetizable software headcount, ultimately eroding lock-in, increasing churn, and reducing growth for SaaS incumbents. Compounding this risk further is the concern that legacy SaaS incumbents will find it hard to change their seat-based pricing model vs. many AI-native companies are pricing based on outcomes or consumption from Day 1.

-

Disruption to customer acquisition channels: SaaS incumbents who have traditionally relied on digital marketing strategies such as SEO to drive traffic are now seeing a decrease in the effectiveness of these channels particularly as consumers/customers rely on LLMs for searches and product recommendations.

Market/macro impacts:

-

Investor capitulation hits software: As a consequence of all the concerns outlined above, SaaS investors are now applying lower terminal values, lower free-cash-flow projections, and higher discount rate assumptions. Some investors may even be in a “risk-off” stance in the category due to modeling uncertainty. Volatile sell-offs can serve to fuel a vicious negative cycle (stop-loss triggers, etc.). At the same time, capital is rotating out of SaaS because investors are more excited by AI beneficiaries in adjacent areas such as infrastructure, semiconductors, and energy. All of these factors lead to multiple compression in the SaaS category.

2026’s SaaSacre feels more unsettling than prior pullbacks because there’s no obvious trigger to call a bottom. Whether AI-driven fears are justified or the risks are more idiosyncratic than systematic, pessimism has spread indiscriminately across the SaaS landscape and triggered a broad de-rating. The sector is now confronting fundamental questions about its future and the durability of what was once a highly predictable business model, with growing confusion over which pressures are structural versus merely cyclical. More reflections to come in future posts!